In our latest Emerging Markets Monthly Comments (February 2026), TAC ECONOMICS highlights a major shift in the global risk landscape: overall country risk across Emerging Markets (EM) has declined significantly since its mid-2023 peak.

Our proprietary Country Risk Premium (CRP), a comprehensive measure of macroeconomic, financial, political, governance, and structural risks, shows a 200bps reduction over two years, bringing the EM average to 408bps. This reflects:

- Stronger macro-financial fundamentals

- Reduced external imbalances

- More neutral monetary conditions

- Lower global risk aversion toward EM assets

However, this aggregate improvement masks growing fragmentation. Political and governance risks have risen in many countries, and an exceptional number of EM display early warning signals for potential shocks. In this environment, country selection is more critical than ever.

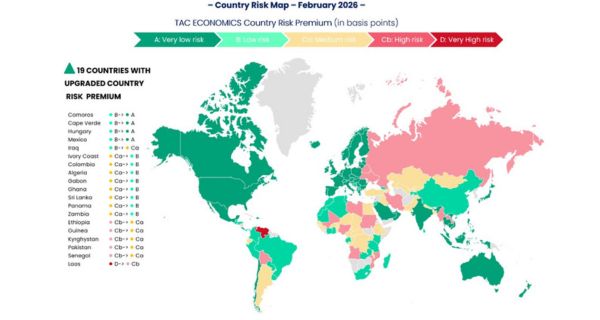

Below, we summarize key trends and illustrate them with selected country cases across major regions.

Central & Eastern Europe: Convergence, but rising dispersion

Central & Eastern Europe has seen a steady improvement in aggregate risk, largely erasing the initial impact of the Russia–Ukraine war. Yet, risk dispersion within the region has widened.

- Poland: The CRP fell sharply to around 109bps, reflecting improved macro-financial conditions and stronger governance indicators. Nonetheless, geopolitical sensitivity remains elevated due to proximity to the war in Ukraine.

- Czech Republic: Now at a record-low CRP (63bps), supported by stronger growth dynamics and restored policy credibility.

- Turkey: Despite some improvement, risk remains elevated (464bps). Persistent inflation, limited FX reserve rebuilding, and renewed pressures in economic and political risk ratings constrain further progress.

- Montenegro: Significant CRP reduction, but early warning signals on activity and solvency highlight sensitivity to capital flows and commodity price volatility.

Overall, while macro resilience has strengthened, cyclical and geopolitical vulnerabilities remain key transmission channels of risk.

Central & Eastern Europe: Convergence, but rising dispersion

Central & Eastern Europe has seen a steady improvement in aggregate risk, largely erasing the initial impact of the Russia–Ukraine war. Yet, risk dispersion within the region has widened.

- Poland: The CRP fell sharply to around 109bps, reflecting improved macro-financial conditions and stronger governance indicators. Nonetheless, geopolitical sensitivity remains elevated due to proximity to the war in Ukraine.

- Czech Republic: Now at a record-low CRP (63bps), supported by stronger growth dynamics and restored policy credibility.

- Turkey: Despite some improvement, risk remains elevated (464bps). Persistent inflation, limited FX reserve rebuilding, and renewed pressures in economic and political risk ratings constrain further progress.

- Montenegro: Significant CRP reduction, but early warning signals on activity and solvency highlight sensitivity to capital flows and commodity price volatility.

Overall, while macro resilience has strengthened, cyclical and geopolitical vulnerabilities remain key transmission channels of risk.

Latin America: Macro recovery vs. political pressures

Latin America’s average CRP has declined markedly since 2023, with economic and financial risk ratings returning to long-term averages. Yet, political and governance risks have increased to their highest level in over a decade.

A growing dichotomy is evident:

More resilient economies benefit from:

- Better external balances

- Significant disinflation

- Improved policy credibility

More vulnerable countries face:

- External debt constraints

- Liquidity pressures

- Elevated socio-political tensions

Illustrative cases:

- Colombia: Now in the low-risk category, supported by improved external accounts, stronger reserves, and robust domestic demand indicators.

- Peru: Solid macro framework and mining-driven growth but increasing institutional fragmentation and electoral uncertainty are overtaking macro strengths.

- Mexico: Economic risk is low and improving, yet political and geopolitical vulnerabilities, especially linked to relations with the U.S., limit the overall decline in risk pricing.

The region illustrates clearly how political variables are increasingly driving risk differentiation.

Asia: Low average risk, deep fragmentation

Asia maintains one of the lowest average CRPs (373bps), with several countries in the very low-risk category. Yet fragmentation is pronounced.

- China: CRP remains broadly stable (398bps), but a new Watch List indication on economic activity signals heightened cyclical risks from late 2026 onward, with possible financial spillovers.

- Pakistan: Significant CRP reduction thanks to rebounding growth and improved risk premiums. However, external fragilities, weak buffers, and political tensions persist.

- Laos: Although risk has fallen dramatically from extreme levels, structural vulnerabilities remain acute (high external debt, weak reserves).

Core ASEAN economies and India continue to benefit from resilient domestic demand and contained macro-financial risk.

In Asia, exposure to China, domestic political dynamics, and policy credibility create sharply differentiated trajectories.

Middle East & North Africa (MENA): GCC anchors vs. fragile periphery

The MENA region’s average CRP has improved to 391bps, largely driven by hydrocarbon-rich GCC economies implementing credible economic reforms.

- Oman: Now among the lowest-risk EM (178bps), supported by strong macro fundamentals, limited public debt, and improved governance metrics.

- Morocco: Strong improvement in both economic and governance indicators; GDP growth expected above 4% in 2026–2027, supported by rising reserves and vanishing inflation.

- Egypt: Risk has declined steadily following the 2024 currency devaluation, which restored competitiveness, though political risk remains elevated.

However, structural divergence remains wide between reform-oriented GCC anchors and fragile economies facing socio-political and financial pressures.

Sub-Saharan Africa: Structural vulnerabilities persist

Sub-Saharan Africa has also benefited from lower global risk aversion, with average CRP declining by 200bps since 2023. Yet, the region remains above the global EM average and displays widening dispersion.

Persistent vulnerabilities include:

- External deficits

- Limited FX reserves

- Debt servicing stress

- Political instability

Country highlights:

- Ghana: Major improvement in both macro-financial and governance metrics, supported by tighter monetary policy, disinflation, and stronger reserves.

- Ivory Coast: Strengthened fiscal and external positions, supported by IMF and World Bank engagement, contributing to a medium-risk profile.

- Nigeria: Risk remains structurally high despite ambitious reforms, due to governance gaps, rising debt, and banking system FX exposure.

- South Africa: Relatively resilient profile thanks to diversified economy, deep financial markets, and stronger institutional capacity.

The region underscores the importance of institutional strength and policy credibility as amplifiers or mitigators of macro-financial pressures.

Conclusion

Emerging Markets have entered a new phase:

- Lower aggregate risk

- Improved macro-financial resilience

- Declining global risk aversion

But also:

- Rising political and governance fragilities

- More frequent early warning signals

- Widening intra-regional divergence

In this context, EM investment strategies cannot rely on regional averages. Structural resilience, institutional credibility, and shock-absorption capacity are now decisive factors in differentiating risks — and opportunities — across countries.

At TAC ECONOMICS, our Country Risk Premium framework provides investors and corporates with the tools to navigate this increasingly fragmented EM landscape with precision and forward-looking insight.